Systematic corporate credibility assessment is defined as the structured process by which regulators evaluate whether a company's public disclosures, governance structures, and operational controls accurately reflect its actual conduct and performance. For corporate regulators and compliance professionals, this process is no longer discretionary. The UK Financial Conduct Authority, the European Securities and Markets Authority, and India's Securities and Exchange Board of India have each developed formal frameworks that treat credibility evaluation as a core supervisory function. The regulatory credibility frameworks now converging across jurisdictions share three foundational pillars: methodology transparency, governance accountability, and conflict of interest management.

What are the key components of a systematic corporate credibility assessment framework?

A credibility assessment framework is defined by four structural components: governance and oversight, methodology transparency, conflict of interest controls, and operational quality management. Each component addresses a distinct failure mode in corporate disclosure. Together, they form the evidentiary architecture that regulators use to distinguish genuine accountability from engineered narrative.

Governance and oversight establish who is responsible for credibility determinations and how that responsibility is enforced. Governance structures must assign named accountability for methodology formulation, rating application, and quality review. Without named accountability, credibility assessments become collective exercises with no individual ownership.

Methodology transparency requires that the criteria, data sources, weighting logic, and known limitations of any credibility or ratings process be disclosed publicly. The FCA's ESG Ratings Providers regime is built explicitly around this requirement, mandating that firms publish the full basis of their rating methodologies, including data source limitations. Transparency without specificity is insufficient. Disclosures must be granular enough for an informed third party to replicate the analytical logic.

Conflict of interest management identifies and mitigates situations where the rating or assessment entity has a financial or relational interest in the outcome. This includes relationships between rating providers and rated entities, shared ownership structures, and advisory service bundling.

Operational controls cover quality assurance, record keeping, and outsourcing restrictions. The FCA prohibits outsourcing operational responsibility for the ESG ratings process, requiring firms to maintain internal control over methodology application. This prohibition exists because outsourced execution severs the chain of accountability between published methodology and actual scoring decisions.

- Governance: Named accountability for methodology and rating decisions

- Transparency: Public disclosure of criteria, data sources, weights, and limitations

- Conflict management: Identification, disclosure, and mitigation of material conflicts

- Quality controls: Internal review processes, version control, and audit trails

- Record keeping: Documented evidence that methodology was applied as described

- Outsourcing restrictions: Prohibition on delegating core credibility functions externally

Pro Tip: Enforce process ownership at the point of methodology application, not just at the point of publication. A methodology document that no named individual is accountable for executing is a transparency exercise, not a credibility control.

How do regulatory frameworks across jurisdictions address corporate credibility?

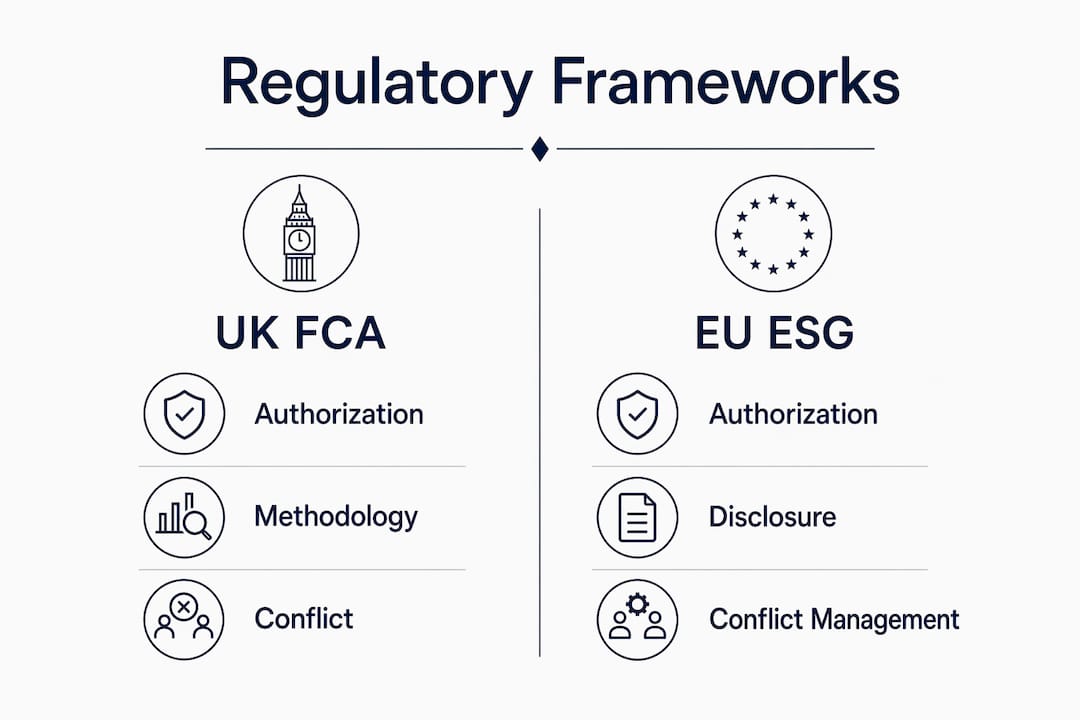

Three major regulatory regimes have formalized corporate credibility evaluation into enforceable frameworks. Each reflects different market structures and legal traditions, yet all converge on the same core requirements: authorization, methodology disclosure, conflict management, and ongoing supervision.

The UK FCA is consulting on detailed requirements for ESG Ratings Providers through end of 2025, with the regime centered on governance, systems, controls, and transparency. The FCA's approach treats credibility as an ongoing operational standard, not a one-time authorization condition. Firms must demonstrate that their internal controls produce consistent, documented application of their stated methodologies.

The EU ESG Ratings Regulation establishes a cross-border authorization framework applying from 2 July 2026. It requires public disclosure of rating methodologies via websites and marketing communications, and it applies to any provider operating in EU markets regardless of domicile. The EU framework is notable for its extraterritorial reach and its explicit requirement that methodology disclosures appear in marketing materials, not just regulatory filings.

India's SEBI takes a structurally distinct approach. SEBI anchors part of its Core ESG ratings to third-party assured disclosures, specifically the Business Responsibility and Sustainability Report Core parameters. By tying ratings to independently verified inputs, SEBI reduces the scope for contested methodological judgments and creates an evidence hierarchy that regulators can audit directly.

| Regulatory Component | UK FCA | EU ESG Ratings Regulation | India SEBI |

|---|---|---|---|

| Authorization requirement | Yes, regime under development | Yes, from July 2026 | Yes, mandatory registration |

| Methodology disclosure | Required, including limitations | Public website and marketing | Required, with BRSR Core anchor |

| Conflict of interest rules | Explicit prohibition and management | Governance-level requirements | Disclosure and mitigation rules |

| Outsourcing restrictions | Prohibited for core functions | Governance accountability retained | Internal control requirements |

| Assured disclosure anchor | Not specified | Not specified | BRSR Core parameters |

| Ongoing supervision | FCA supervisory oversight | ESMA authorization and review | SEBI periodic review |

The commonalities across these three regimes are more instructive than their differences. All three require methodology disclosure. All three mandate conflict management. All three impose governance accountability on named internal functions. This convergence signals that regulatory credibility frameworks are moving toward a global baseline, even without formal harmonization.

What challenges arise in implementing credibility assessment frameworks?

Implementation of corporate credibility evaluation frameworks surfaces three categories of failure that regulators must anticipate and design against.

The first is the credibility gap, which manifests in three distinct forms. A Reasonable Gap reflects legitimate methodological disagreement where two credible analysts reach different conclusions from the same data. A Deficient Standard Gap occurs when the methodology itself is inadequate, regardless of how faithfully it is applied. A Deficient Performance Gap occurs when a sound methodology is applied inconsistently or selectively. A 2026 study on ESG assurance users found that stakeholder trust fully mediates the link between expectation gaps and perceived credibility, with Deficient Performance having the strongest negative impact on trust. This finding means that execution failures damage credibility more severely than methodological disputes.

The second challenge is transparency opacity. Published methodologies can satisfy disclosure requirements while leaving actual scoring decisions entirely opaque. Without process ownership constraints, transparency becomes a paper exercise. The FCA's prohibition on outsourcing core functions directly addresses this failure mode by requiring that the entity publishing the methodology also controls its application.

The third challenge is contested ESG criteria. Many corporate credibility dimensions, particularly in environmental and social domains, involve genuinely contested normative judgments. Regulators must design frameworks that acknowledge this contestation without allowing it to become a shield against accountability. SEBI's approach of anchoring ratings to assured BRSR Core parameters reduces this problem by limiting the scope of discretionary judgment to areas where third-party verification already exists.

- Deficient Performance gaps are the most trust-damaging credibility failure type

- Methodology transparency without process ownership produces disclosure opacity

- Contested criteria require bounded discretion, not unlimited methodological flexibility

- Trust mediates between expectation gaps and credibility perception at the stakeholder level

Pro Tip: Design credibility frameworks with iterative review cycles built in. Contested ESG criteria evolve as science, regulation, and market norms develop. A framework that cannot be updated without full reauthorization will become structurally obsolete within two to three reporting cycles.

How can regulators operationalize corporate credibility assessment effectively?

Operationalizing a systematic credibility review requires moving from framework design to enforcement architecture. The following sequence reflects best practice drawn from the FCA, SEBI, and UK Financial Reporting Council models.

-

Separate methodology description from demonstrated application. A credible assessment framework treats governance, systems, controls, and record keeping as evidentiary bridges between what the methodology says and what the entity demonstrably did. Regulators should require firms to produce both the methodology document and the governance records showing how it was applied in specific rating decisions.

-

Anchor ratings to third-party assured disclosures where available. SEBI's use of BRSR Core parameters demonstrates that tying credibility assessments to independently verified inputs reduces both methodological contestation and evidentiary burden on regulators. Where assured disclosures exist, they should form the baseline layer of any corporate credibility evaluation.

-

Implement audit oversight models. The UK Financial Reporting Council operationalizes credibility through continuous monitoring and enforceable oversight structures that extend well beyond initial authorization. Regulators should adopt analogous models that treat credibility as an ongoing supervisory condition, not a one-time gate.

-

Conduct readiness assessments before authorization submissions. Firms seeking authorization under the FCA or EU regimes should complete internal gap analyses against published framework requirements before submission. Regulators benefit from requiring structured readiness declarations that identify known deficiencies and remediation timelines.

-

Require stakeholder engagement disclosures. Credibility frameworks that operate without structured stakeholder input are vulnerable to capture by the rated entity's preferred framing. Regulators should mandate that methodology reviews include documented consultation with data users, including institutional investors, governance advocates, and financial journalists.

-

Apply sector-specific benchmarks to calibrate credibility thresholds. Credibility standards appropriate for a financial services firm differ from those applicable to a manufacturing company. Sector benchmarking allows regulators to apply consistent methodology while accommodating material differences in disclosure norms and data availability.

Key takeaways

Effective corporate credibility assessment requires regulators to enforce governance accountability, methodology transparency, and process ownership simultaneously, not sequentially.

| Point | Details |

|---|---|

| Framework components | Governance, methodology transparency, conflict management, and operational controls form the four pillars of credible assessment. |

| Jurisdictional convergence | FCA, EU ESG Ratings Regulation, and SEBI all require methodology disclosure, conflict management, and named governance accountability. |

| Execution gaps are most damaging | Deficient Performance gaps reduce stakeholder trust more severely than methodological disagreements or standard deficiencies. |

| Transparency requires process ownership | Published methodologies without internal control over application produce disclosure opacity, not genuine credibility. |

| Assured disclosures anchor credibility | Tying assessments to third-party verified inputs, as SEBI does with BRSR Core, reduces contestation and strengthens evidentiary integrity. |

Where regulatory credibility frameworks still fall short

The frameworks described in this article represent genuine progress. The FCA's prohibition on outsourcing core credibility functions, SEBI's evidence hierarchy anchored to assured disclosures, and the EU's extraterritorial authorization regime each address real failure modes that prior voluntary codes ignored entirely.

What concerns me is the gap between framework design and enforcement capacity. Most regulatory bodies can assess whether a methodology document exists and whether it contains the required disclosures. Far fewer have the forensic capacity to determine whether the methodology was actually applied as described in specific rating decisions. That gap is where credibility failures live.

The trust mediation research makes this concrete. Stakeholders do not primarily lose confidence in credibility frameworks because the methodology is wrong. They lose confidence because they observe outcomes that the methodology cannot explain. Regulators who focus enforcement resources on disclosure completeness while neglecting execution consistency will produce frameworks that satisfy legal requirements without restoring market trust.

The next generation of credibility regulation needs to invest in forensic review capacity, not just disclosure mandates. That means training supervisory staff to read governance records as evidence of execution, not just as compliance artifacts. It means building credibility scoring methodologies that can be applied consistently across sectors and reporting cycles. And it means accepting that iterative regulatory design, with built-in review cycles and stakeholder input mechanisms, is not a sign of framework weakness. It is the only design that can keep pace with contested and evolving corporate disclosure norms.

— Glen

How Lacunaindex supports corporate credibility assessment

Regulators and compliance professionals who need a structured, evidence-based process for evaluating corporate credibility will find Lacunaindex's forensic methodology directly applicable to the frameworks described in this article.

Lacunaindex measures the gap between corporate narrative claims and actual delivery using only public records, including SEC filings, earnings calls, proxy statements, and press releases. The platform's credibility scoring methodology applies the same separation of declared methodology from demonstrated application that the FCA and SEBI frameworks require of rated entities. For regulators building or stress-testing their own assessment frameworks, the Lacunaindex user guide provides a structured walkthrough of how execution scores, aspiration-to-execution gaps, and sector benchmarks are constructed and interpreted from public disclosure data alone.

FAQ

What is systematic corporate credibility assessment?

Systematic corporate credibility assessment is the structured regulatory process of evaluating whether a company's disclosures, governance, and controls accurately reflect its actual conduct. It applies consistent methodology across governance, transparency, conflict management, and operational controls to produce defensible credibility determinations.

How does the EU ESG ratings regulation affect corporate credibility oversight?

The EU ESG Ratings Regulation, applying from 2 July 2026, requires authorization, methodology disclosure, and conflict management from all providers operating in EU markets. It mandates that rating methodologies appear in public website disclosures and marketing communications, not only in regulatory filings.

What is the difference between a deficient standard and a deficient performance gap?

A Deficient Standard Gap occurs when the assessment methodology itself is inadequate. A Deficient Performance Gap occurs when a sound methodology is applied inconsistently or selectively. Research shows Deficient Performance gaps cause the greatest damage to stakeholder trust and perceived credibility.

Why does the FCA prohibit outsourcing core credibility functions?

The FCA prohibits outsourcing operational responsibility for ESG ratings processes because outsourced execution severs accountability between a published methodology and actual scoring decisions. Internal control over methodology application is the mechanism that converts transparency disclosures into enforceable credibility standards.

How does sebi's approach differ from the UK and EU frameworks?

SEBI anchors part of its Core ESG ratings to third-party assured BRSR Core disclosures, creating an evidence hierarchy that reduces methodological contestation. The UK and EU frameworks focus primarily on governance and disclosure requirements without specifying an assured disclosure anchor as a credibility baseline.